Insurance Every Independent Caregiver in the UK Should Have

(and Where to Get It)

There’s a quiet myth in independent care work:

“I’m careful. I’ve never had a complaint. I don’t need insurance.”

Until the day you do.

Insurance isn’t about expecting something to go wrong.

It’s about protecting your livelihood when it does.

And as independent carers — without an agency shielding us — that protection becomes personal.

💬 Why Insurance Matters More Than You Think

As a self-employed carer, you are:

Your own HR department

Your own legal team

Your own risk manager

Your own safety net

If a client falls and blames your guidance…

If you accidentally damage expensive flooring…

If a family alleges negligence…

If you injure yourself and can’t work…

There is no agency stepping in.

That’s why this matters.

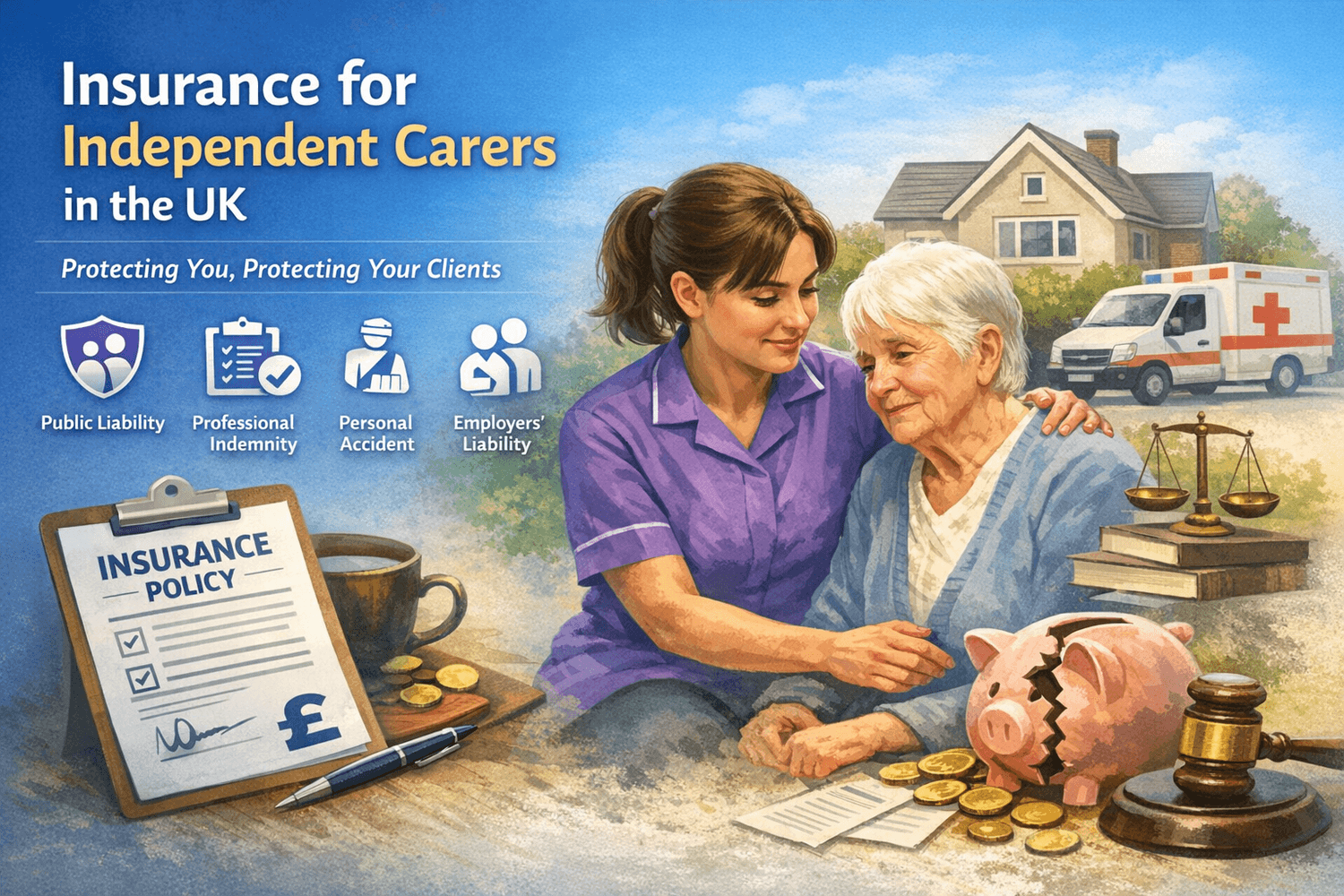

🔎 The Core Covers Independent Carers Should Consider

1️⃣ Public Liability Insurance

This covers you if a client or third party claims injury or property damage due to your work.

Example:

A client trips over equipment you moved.

You spill hot tea and damage furniture.

A family alleges unsafe practice.

Most specialist policies offer up to £5 million cover.

Not legally required — but professionally essential.

2️⃣ Professional Indemnity Insurance

This protects you if someone claims your professional advice or actions caused harm.

Example:

Medication prompting advice is questioned.

A risk assessment decision is challenged.

Care planning advice is disputed.

If you operate independently and make judgement calls, this cover matters.

3️⃣ Personal Accident Cover

If you are injured while working and cannot earn?

No shifts = no income.

Personal accident cover provides financial support if you're unable to work due to injury.

Especially important for live-in carers.

4️⃣ Employers’ Liability Insurance

Legally required if you employ anyone, even casually.

If you hire:

A second carer

A relief carer

Administrative help

You must have this cover.

🏆 Reputable UK Insurance Providers for Independent Carers

Below are specialist providers commonly used by UK self-employed carers.

🟣 Carer Insure

Designed specifically for carers & personal assistants

Public liability up to £5m

FCA regulated

Straightforward online policies

Good option for sole carers starting out.

🟣 Surewise

Popular among self-employed carers

Monthly payment options

Often includes legal expenses

Personal accident add-ons available

Well known in the Direct Payments space.

🟣 Marsh Commercial

Specialist care sector insurance

Risk advice support

Tailored policies

More consultative — useful for complex roles.

🟣 Fish Insurance

Carer & PA insurance

Optional motor extensions

Legal defence cover

Often used by carers who drive clients.

🟣 Superscript

Flexible online insurance

Customisable cover

Broader healthcare professional policies

Good for carers expanding into consultancy or training.

⚠️ What Happens Without Insurance?

This is the uncomfortable bit.

If a claim is made against you personally:

Legal defence can cost thousands

Compensation claims can reach tens of thousands

Even unfounded allegations require representation

Without cover, it’s your savings, your home, your income at risk.

Independent means freedom.

But freedom without protection is vulnerability.

💡 Common Carer Misconceptions

“The family has insurance.”

Their home insurance does not cover your professional liability.

“I’ve never had a complaint.”

Insurance isn’t about past performance — it’s about future unpredictability.

“It’s too expensive.”

Many policies start from the cost of one hour’s work per month.

One hour of earnings for peace of mind.

🧭 How to Choose the Right Policy

Before buying, ask:

What is my level of public liability cover?

Does it include professional indemnity?

Are legal expenses included?

Am I covered for live-in placements?

Am I covered to administer medication?

Does it include personal accident protection?

Read exclusions carefully.

Care roles vary — make sure your policy matches your reality.

💜 Why This Matters (JCC Perspective)

At JCC, we champion independence.

But independence isn’t just about:

Setting your rates

Choosing your clients

Avoiding agency fees

It’s about operating as a professional. And professionals protect themselves.

Insurance isn’t fear-based. It’s empowerment.

It says:

“I take my role seriously.”

“I protect my clients.”

“I protect myself.”

“I am building something sustainable.”

📌 The Bottom Line

If you are self-employed in care, insurance isn’t optional in spirit — even if not legally required in all cases.

It protects:

Your income

Your reputation

Your confidence

Your future

And when you’re building independence, that matters.

If you’re a carer navigating pricing, boundaries, or professionalism in independent care — you’re not alone. This is exactly why communities like Just Care Community exist.